Michael T. Belongia

Peter Ireland

In

December 2015, after keeping its federal funds rate target close to

zero for more than seven years, the Federal Open Market Committee (FOMC)

finally achieved “lift off,” raising the target to a range between 0.25

and 0.50 percent. The Committee maintained that very low range for

nearly all of 2016, waiting until last month before bringing the target

rate up another notch, to its current band between 0.50 and 0.75

percent. Will the Fed raise rates more quickly in 2017? Our own

analysis of monetary conditions suggests that the FOMC would be advised

to continue moving gradually instead.

Minutes from the FOMC’s December 2016 meeting

summarize the reasons for the second rate hike, with direct reference

to the Fed’s dual mandate of maximum employment and stable prices.

The

unemployment rate has fallen to 4.7 percent, a value quite close to

current estimates of the natural rate of unemployment. Most FOMC

members view the natural rate as a threshold beyond which further

reductions in unemployment will exert upward pressure on inflation.

Thus, while inflation itself, measured at 1.4 percent using the Fed’s

preferred price index for consumer expenditures, remains below the

FOMC’s announced target of two percent, low unemployment has

strengthened Committee members’ confidence that inflation will return to

a value much closer to target in 2017. Indeed, projections accompanying the FOMC minutes indicate that several additional interest rate increases can be expected in the year ahead.

Clearly,

the FOMC’s strategy continues to be shaped by the belief that the

Phillips curve relation describes a tight link between unemployment and

inflation – an idea we disputed in a previous column for E21.

The FOMC’s strategy rests importantly, as well, on the idea that

interest rates serve most reliably as indicators of the stance of

monetary policy, with continued low rates signaling that policy remains

exceptionally accommodative. Monetarist economists such as Milton

Friedman often point out, however, that interest rates can provide a

misleading view of the effects that monetary policy is having on the

economy especially when inflationary expectations have become unstable.

Most famously, during the Great Depression, Fed policymakers mistakenly

took very low interest rates to mean that they were doing all they

could to support an economic recovery. But a sharp contraction in

measures of money showed, more correctly, that monetary policy was

excessively tight, exacerbating rather than ameliorating the economic

downturn.

Our own recent research

outlines an alternative approach that uses the quantity theory and

measures of money to gauge the stance of monetary policy, which we

propose as a cross-check against more popular analyses built on the

Phillips curve and interest rates instead. Our empirical framework is

organized around two observable variables: the Divisia MZM money supply

as the measure of M on the left-hand side of the quantity equation MV =

PY and nominal GDP as the measure of PY on the right. Because nominal

income is, by definition, the product of real GDP (Y) and the aggregate

price level (P), it conveniently summarizes in one variable both sides

of the dual mandate: maximizing output or employment and stabilizing

prices.

Since

2011, Divisia MZM has grown at an annual rate between 6 and 7 percent,

while nominal GDP has expanded by only 3.5 to 4 percent per year. This

comparison reveals that, instead of remaining constant as the simplest

version of the quantity theory assumes, monetary velocity V has trended

slowly downward over this period. Our approach tracks these changes in V

to estimate, in real time, the long-run value V* towards which actual

velocity appears to be gravitating. We use this estimate of V*,

together with the data on Divisia MZM, to compute the target Q* = MV*

towards which nominal income itself will converge. When the gap between

Q* and PY is positive, it indicates that past money growth is putting

upward pressure on PY; accelerating nominal income growth will then

close the gap. Conversely, when Q* is below PY, past monetary restraint

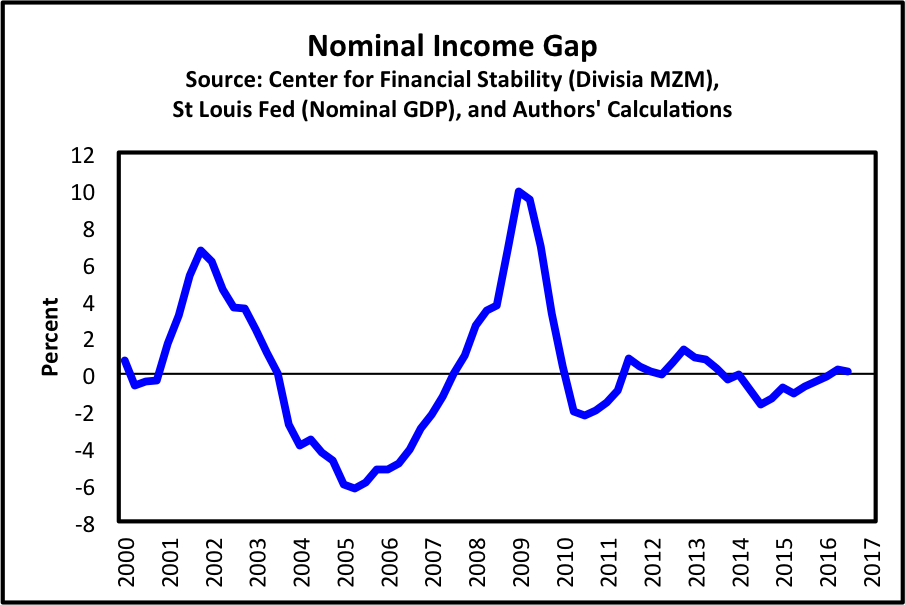

is putting downward pressure on nominal income. The figure below plots

this “nominal income gap” since 2000.

|

By

our measure, monetary policy went from accommodative following the 2001

recession to highly contractionary before the financial crisis of

2007-08. And while policy was appropriately expansionary during the

crisis and recession that followed, its stance since 2010 appears

approximately neutral. This observation leads us to believe that

nominal GDP growth is unlikely to accelerate markedly in 2017. Assuming

that FOMC members are content with nominal GDP growth between 3.5 and 4

percent – which, when split evenly, implies rates of real GDP growth

and inflation between 1.75 and 2 percent – monetary policy seems

well-balanced now. If, however, the FOMC follows through with its plans

to raise interest rates further this year, our monetary cross-check may

provide early warning that they are moving too fast.

No comments:

Post a Comment